Berachain: Risk Management and Survival Code

1. Introduction

As the memecoin market fades, interest in DeFi has begun to increase. Under this trend, the Berachain ecosystem, which has low token volatility and offers high returns, has also begun to attract new users.

From the release of the Berachain mainnet on February 6, 2025 to the writing of this article on March 4, Berachain’s TVL has steadily increased, reaching $3.2 billion, surpassing Base in the overall TVL ranking, and ranking sixth overall.

TVL Trend Berachain; Source: Defi Flame

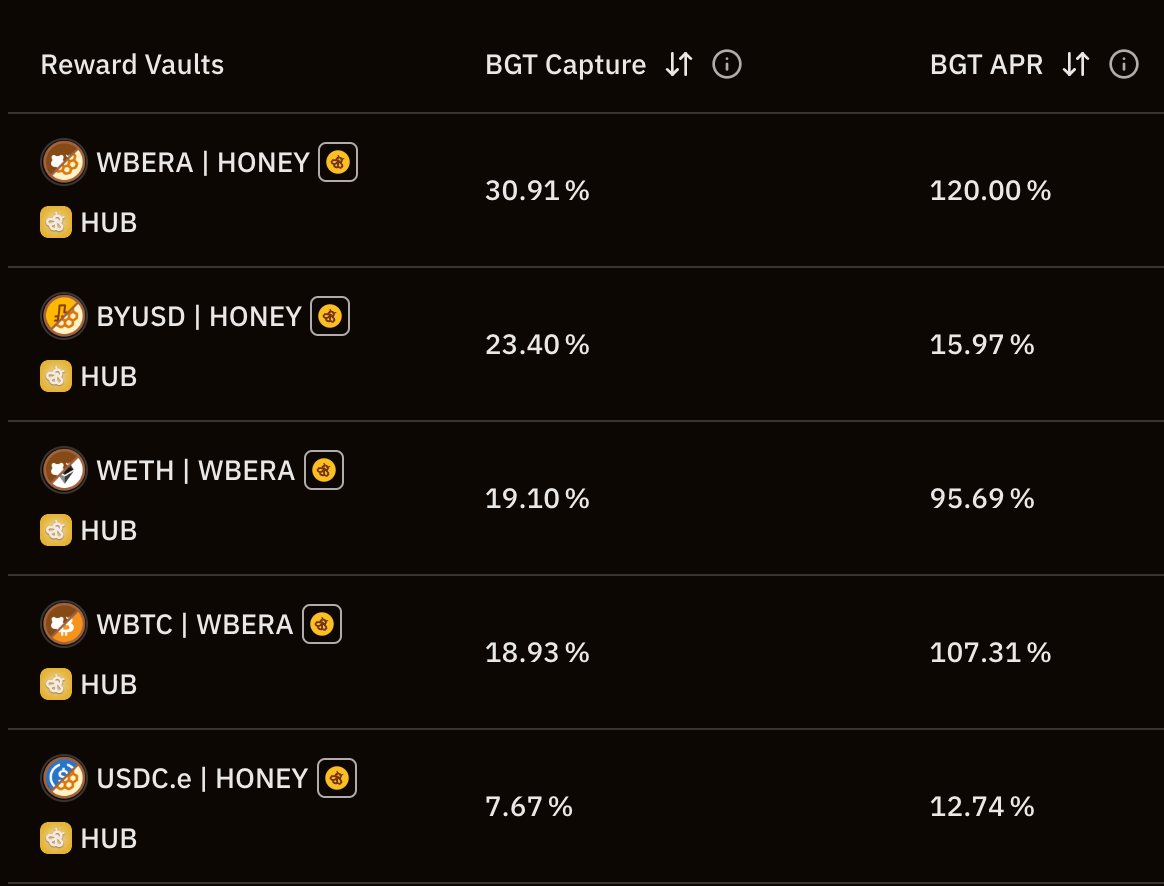

Kodiak、Yeet and Ramen Finance Ecological core projects such as these have been prepared since the Berachain testnet stage and have been launched one after another after the launch of the Berachain mainnet. However, these ecological protocols have not yet been registered in the reward vault that issues $BGT, and currently only BeraSwap Provide liquidity within five liquidity pools to earn $BGT.

Reward Vaults List; Source: Be connected

Users can provide liquidity to the BeraSwap liquidity pool, receive LP tokens, and deposit them Infrared and Stride After there is a protocol that supports liquid $BGT, the received liquid $BGT tokens can be used in other DeFi protocols. Additionally, users can also deposit the same LP tokens to liquidity aggregators Beradrome In order to obtain Beradrome’s native token $BERO, and by staking $BERA, you can obtain rewards accumulated in Beradrome, thereby realizing various ecological participation strategies.

Additionally, the first phase of Berachain governance (Governance Phase 1) started requesting ecosystem protocol reward vault registration on February 26. As these requests are integrated into the protocol and protocol rewards are paid to validators, Berachain’s ecological gameplay is expected to become more diversified. In this process, the role of $BGT, which has the authority to receive rewards and distribute network rewards, will become more important, and the flywheel based on the PoL (Proof of Liquidity) structure will also be activated, leading to the influx of more users and liquidity into Berachain.

In this article, we will look at the Berachain flywheel structure in detail to assist new users in managing risks, and discuss the underlying risks of the Berachain flywheel as well as preventive measures.

2. Understand the Berachain flywheel

Berachain adopts a PoL structure, and network participants such as validators, ecological protocols, and liquidity providers must propose and provide value to each other.

Each participant in the network forms a state of incentive alignment, and the growth and decline of each role is directly related to each other. When each participant has a positive impact on other participants, the following virtuous flywheel operates:

- As the ecosystem grows and expands, the incentives paid by the protocol to validators will also increase.

- As the rewards distributed to $BGT holders increase, the need to obtain $BGT by providing liquidity increases, the need to burn $BGT decreases, and the issuance of $BERA will decrease.

- As liquidity supply increases, the overall ecosystem grows and expands.

When this benign flywheel operates, the price of $BERA, the TVL of the ecological protocol, and the overall ecological profit will increase, allowing all ecological participants to benefit from it. However, for the flywheel to operate smoothly, the following three conditions must be met:

- Loss of protocol reward payouts < Protocol profit from payout rewards and guaranteed liquidity

- Volatility risk exposed by buying/holding ecological tokens < $BGT profit from providing liquidity

- Volatility risk exposure from holding $BERA < Bonus profit from delegating $BGT

When the above conditions are met, the flywheel will begin to operate. Once set in motion, each condition has a positive impact on the others, giving the flywheel effect a way to keep spinning, and the flywheel’s robustness and strength depend on how well the conditions are met.

This flywheel structure of Berachain seems to be a unique feature and advantage not found in other PoS structures, but when one of the conditions cannot be met for a specific reason (and cannot be restored to the original state in the short term), then these conditions will start to have a negative impact on the other conditions, and the flywheel will run in reverse as follows:

- As the ecosystem shrinks, the rewards paid by the protocol to validators decrease.

- As rewards distributed to $BGT holders decrease, the need to acquire $BGT by providing liquidity decreases, the need to burn $BGT increases, and the issuance of $BERA increases.

- As liquidity supply decreases, the ecosystem shrinks.

In this reverse flywheel state, the price of $BERA, the TVL of the ecological protocol, and the overall profit of the ecosystem will decrease until the conditions for flywheel operation are met again.

If we only consider the demand within the ecosystem in the near future, 1) it is expected that there will be many protocols seeking to issue their own tokens as rewards; 2) since the emission of $BGT has just started, the farming efficiency of each $BGT is very high, so the demand for providing liquidity and accumulating $BGT will be relatively high。

For these reasons, Flywheel is likely to operate in the early stages of the mainnet launch, but factors such as macro markets and investment trends in other industries will also affect the operation of Flywheel, so it is difficult to say whether Flywheel will operate successfully.

Next, we will explore several risk factors and scenarios that may trigger the reverse flywheel during the period of flywheel operation.

3. Reverse flywheel plot

3.1. $BERA crash

$BERA plays the following key roles in the Berachain ecosystem:

- Staking for running a node

- Guaranteed minimum value of $BGT

- Used as a deposit asset in various liquidity pools

Therefore, the downward trend in the value of $BERA can also be seen as a weakening of network security, a decrease in the minimum value of $BGT, and a decrease in ecological liquidity. For participants in the Berachain network, the price of $BERA plays a more important role than the price of mainnet tokens for participants in other networks.

When the flywheel is running smoothly, even if the price of $BERA falls to some extent, demand for $BERA can continue to be created if the incentive yield is maintained. But on the contrary, the decline in the value of $BERA may have a negative impact on the ecological protocol, reducing the incentive yield, causing users’ demand to burn $BGT to exchange for $BERA, or to remove the $BERA supplied to the liquidity pool and sell it on the market. This could be the start of a reverse flywheel, causing the value of $BERA to drop again.

Therefore, we should pay special attention to the following situations:

3.1.1. Large-Scale $BERA Unlocking

In addition to $BERA issued through $BGT burning, there is also a planned $BERA unlocking plan, with a total issuance amount of 500M, and the unlocking schedule is as follows:

$BERA Unlock Schedule; Source: Berachain Docs

The linear unlocking plan for investors, early core contributors, and independent community allocations will begin in February 2026, one year after the launch of the mainnet. Prior to this, factors that may trigger selling pressure in the market due to increased $BERA liquidity in the short term include:

- Allocations received by the protocol and community through the RFB program (approximately 2.04% of total issuance)

- Quotations to be allocated through the Boyco program (approximately 2% of total issuance)

Among them, the amount distributed by the protocol and the community to users through the RFB program must have a distribution period of at least 6 months, and since the distribution time of each protocol will be different, it is not expected to cause significant selling pressure on the market in a short period of time.

However, Boyco’s distribution amount is expected to be distributed in approximately 2 months, in a manner similar to current airdrops. In this case, $BERA equivalent to approximately 2% of the total issuance would be supplied to the market, potentially causing selling pressure. In addition, assets deposited in the Boyco plan will also be unlocked when the $BERA airdrop is distributed, which may lead to a reduction in liquidity within the ecosystem. This will create a favorable environment to trigger a reverse flywheel, causing $BERA price and ecological liquidity to decline simultaneously.

Therefore, it will be important to see whether Eco can establish an attractive flywheel before the end of the Boyco plan to effectively absorb the liquidity of $BERA and Eco released into the market.

3.1.2. Mass exit and panic selling of $BGT holders

To earn $BGT, users must deposit liquidity into a liquidity pool capable of issuing BGT rewards and invest sufficient time. However, by BeraHub of Redeem Function, users can burn the $BGT delegated to the validator at any time and obtain $BERA for sale, which only takes about 5 hours to unlock.

Berachain requires an Unboost time of about 5 hours; Source: BeraHub

If users who hold a large amount of $BGT exit the ecosystem at the same time, the circulation of $BERA may increase rapidly. If the price of $BERA drops sharply in a short period of time, it may induce panic selling by other $BGT holders and users who provide $BERA liquidity, leading to a larger decline. Therefore, it is necessary to monitor the burn volume trend of $BGT to understand the dynamics of the current ecosystem.

$BGT Emission & Burn Trend; Source: @thj

Additionally, the reward rate and $BGT yield trends by providing liquidity are the most critical factors in determining $BGT burning and delegation demand. By continuing to observe each trend, it is possible to predict, to a certain extent, the potential risk scenarios that trigger the above mentioned, as well as the likelihood of flywheel recovery if a massive $BGT burn occurs.

At the same time, the demand for liquid $BGT tokens will increase as the incentive rate increases, causing the price to rise; and as the incentive rate decreases, the demand will decrease, and the price will decrease. Therefore, if it is difficult to obtain data on past reward rates and $BGT yields, its approximate value can be estimated by the premium trend of liquid $BGT relative to $BERA, which reflects the intrinsic value of $BGT.

iBGT/B

ERA Price Chart; Source: Dex Screener

However, the price of liquid $BGT tokens is affected not only by the intrinsic value of $BGT, but also by how incentives are distributed in the liquidity protocol and protocol-related factors, so these factors should also be considered together.

3.2. Slowing inflation and growth

In addition to the 500M $BERA distributed to network participants within three years of mainnet launch, Berachain has an annual inflation rate of $BGT of approximately 10%. Although some of the network fees submitted by users will be burned, since Berachain’s main activity is to deposit assets into liquidity pools and collect interest, it is difficult to expect a significant amount to be burned.

This means that even if Berachain establishes a positive flywheel three years from now when all $BERA is unlocked, to sustain it for a year would require a way to attract inflows of external funds that are greater than the inflation rate during that period.

Founder of Berachain Smokey The Bera Accepting Bell Curve interviewmentioned that they are developing a dynamic inflation model that changes based on the reward rate for distributing $BGT to make up for the above issues.

While this feature may help control the acceleration of the flywheel and contribute to the sustainability of development, as long as “inflation” persists, the reverse flywheel leading to the price decline of $BERA and ecological contraction is inevitable at a certain stage. Therefore, even from a long-term perspective, several ecological indicators mentioned above must be continuously monitored to diagnose the current status of the ecology.

In addition, in Berachain, the strategy of simply holding $BERA spot for a long time without utilizing it in the ecosystem is an inefficient investment method and will not be able to recover the value diluted due to “inflation”. Therefore, for users who want to take advantage of $BERA to open a position, depositing it into the ecological protocol to actively generate interest is a very important strategy.

If users want to establish a stable position in the ecosystem for a long time, conservatively using assets less affected by flywheel prices (such as $BTC, $ETH, stablecoins, etc.) to accumulate $BGT or perform double-entry deposit operations may be an effective method.

3.3. Monopoly $BGT

In the PoS structure used by most recently launched mainnets, entities with larger stakes receive greater network rewards. This leads to the consolidation of validator stakes and poses a risk of network centralization.

Validator Staking Market Share in the Ethereum Network; Source: @hildobby

Berachain, which was created by modifying the basic PoS structure, also experienced this phenomenon. In addition, in Berachain, validators holding a large amount of $BGT can directly intervene in the ecosystem and unilaterally design a structure that is beneficial to themselves. Therefore, $BGT monopoly will lead to ecological monopoly. Compared with other PoS-based networks, there will be a greater risk of network token monopoly.

To prevent this problem, the team capped $BERA staking that affects block creation authority to 10M and introduced a method where Boosting inefficiently increases as the amount of $BGT representation that determines the $BGT generated per block increases. However, these limitations can be circumvented by operating multiple nodes distributed by a single entity, or through collusion between multiple validators.

In particular, the Liquidized $BGT protocol has an advantage in attracting liquidity for use in the Berachain Reward Vault, as the potential value of “liquidity” is high and can directly accumulate $BGT on behalf of users by depositing liquidity received from users into the Reward Vault. In addition, by awarding this $BGT back to the nodes they operate or cooperate with, this kind of agreement can obtain a large amount of $BGT emission voting rights without negotiating with other ecological entities.

If these protocols discharge additional $BGT of these voting rights into a liquidity pool containing liquidized $BGT tokens, the liquidized $BGT protocol can set up its own independent flywheel, increasing demand for the liquidity provided to the protocol without even having to pay independent rewards.

In this case, the flywheel of liquifying the $BGT protocol itself becomes as powerful as the ratio of $BGT held by the protocol to the total $BGT issued within the ecosystem. If multiple liquid $BGT protocols obtain a large amount of $BGT in the above-mentioned manner and continue to pursue the direction of only increasing the liquidity supply demand of their own liquid $BGT tokens, it may inhibit the liquidity improvement of other protocols and hinder the launch and development of new protocols, thus limiting the diversity of the ecosystem, ultimately causing the ecological scale to shrink and triggering a reverse flywheel.

As mentioned before, the $BGT monopoly can be structurally restricted through the protocol operating mechanism, but it is difficult to completely block it. Therefore, the most certain way to prevent specific entities from monopolizing the ecology is for participants to reach a consensus on ecological sustainability before the monopoly structure is consolidated, and to continue paying attention and working hard for this consensus in the community.

4. Summary

So far, we have explored how Berachain’s flywheel works, the conditions under which it operates, and the reverse flywheel plot. In addition to the possibilities introduced in this article, the reverse flywheel will also operate if the three conditions for driving the flywheel cannot be met, so it is very important to continue to pay attention to network and ecological indicators to evaluate the operating status of the flywheel in Berachain.

Additionally, unfamiliar PoL mechanisms and the various forms of DeFi protocols that exploit them are combining to create complex derivatives and synthetic assets that are difficult to intuitively understand. Therefore, users need to proactively understand their position structure and be aware of overlapping structural and security risks in advance.

From a long-term perspective, the challenge Berachain faces is to continue to expand the ecosystem while also formulating a strategy to increase network fees to cope with the possibility of a reverse flywheel caused by inflation. It is necessary to pay close attention to whether consumer applications such as Perp DEX or on-chain games can settle in the ecosystem to generate real user traffic beyond “simple deposits”.

I hope this article can clearly help users understand the Berachain ecosystem and effectively respond when the reverse flywheel comes.

Disclaimer:

- This article is reproduced from [DeSpread], and the copyright belongs to the original author [Tranks], if you have any objection to the reprint, please contact Gate Learn team, the team will handle it as soon as possible according to relevant procedures.

- Disclaimer: The views and opinions expressed in this article represent only the author’s personal views and do not constitute any investment advice.

- Other language versions of the article are translated by the Gate Learn team and are not mentioned in Gate.io, the translated article may not be reproduced, distributed or plagiarized.

บทความที่เกี่ยวข้อง

In-depth Explanation of Yala: Building a Modular DeFi Yield Aggregator with $YU Stablecoin as a Medium

What is Stablecoin?

What is Liquidity Farming?

Berachain: Risk Management and Survival Code

1. Introduction

As the memecoin market fades, interest in DeFi has begun to increase. Under this trend, the Berachain ecosystem, which has low token volatility and offers high returns, has also begun to attract new users.

From the release of the Berachain mainnet on February 6, 2025 to the writing of this article on March 4, Berachain’s TVL has steadily increased, reaching $3.2 billion, surpassing Base in the overall TVL ranking, and ranking sixth overall.

TVL Trend Berachain; Source: Defi Flame

Kodiak、Yeet and Ramen Finance Ecological core projects such as these have been prepared since the Berachain testnet stage and have been launched one after another after the launch of the Berachain mainnet. However, these ecological protocols have not yet been registered in the reward vault that issues $BGT, and currently only BeraSwap Provide liquidity within five liquidity pools to earn $BGT.

Reward Vaults List; Source: Be connected

Users can provide liquidity to the BeraSwap liquidity pool, receive LP tokens, and deposit them Infrared and Stride After there is a protocol that supports liquid $BGT, the received liquid $BGT tokens can be used in other DeFi protocols. Additionally, users can also deposit the same LP tokens to liquidity aggregators Beradrome In order to obtain Beradrome’s native token $BERO, and by staking $BERA, you can obtain rewards accumulated in Beradrome, thereby realizing various ecological participation strategies.

Additionally, the first phase of Berachain governance (Governance Phase 1) started requesting ecosystem protocol reward vault registration on February 26. As these requests are integrated into the protocol and protocol rewards are paid to validators, Berachain’s ecological gameplay is expected to become more diversified. In this process, the role of $BGT, which has the authority to receive rewards and distribute network rewards, will become more important, and the flywheel based on the PoL (Proof of Liquidity) structure will also be activated, leading to the influx of more users and liquidity into Berachain.

In this article, we will look at the Berachain flywheel structure in detail to assist new users in managing risks, and discuss the underlying risks of the Berachain flywheel as well as preventive measures.

2. Understand the Berachain flywheel

Berachain adopts a PoL structure, and network participants such as validators, ecological protocols, and liquidity providers must propose and provide value to each other.

Each participant in the network forms a state of incentive alignment, and the growth and decline of each role is directly related to each other. When each participant has a positive impact on other participants, the following virtuous flywheel operates:

- As the ecosystem grows and expands, the incentives paid by the protocol to validators will also increase.

- As the rewards distributed to $BGT holders increase, the need to obtain $BGT by providing liquidity increases, the need to burn $BGT decreases, and the issuance of $BERA will decrease.

- As liquidity supply increases, the overall ecosystem grows and expands.

When this benign flywheel operates, the price of $BERA, the TVL of the ecological protocol, and the overall ecological profit will increase, allowing all ecological participants to benefit from it. However, for the flywheel to operate smoothly, the following three conditions must be met:

- Loss of protocol reward payouts < Protocol profit from payout rewards and guaranteed liquidity

- Volatility risk exposed by buying/holding ecological tokens < $BGT profit from providing liquidity

- Volatility risk exposure from holding $BERA < Bonus profit from delegating $BGT

When the above conditions are met, the flywheel will begin to operate. Once set in motion, each condition has a positive impact on the others, giving the flywheel effect a way to keep spinning, and the flywheel’s robustness and strength depend on how well the conditions are met.

This flywheel structure of Berachain seems to be a unique feature and advantage not found in other PoS structures, but when one of the conditions cannot be met for a specific reason (and cannot be restored to the original state in the short term), then these conditions will start to have a negative impact on the other conditions, and the flywheel will run in reverse as follows:

- As the ecosystem shrinks, the rewards paid by the protocol to validators decrease.

- As rewards distributed to $BGT holders decrease, the need to acquire $BGT by providing liquidity decreases, the need to burn $BGT increases, and the issuance of $BERA increases.

- As liquidity supply decreases, the ecosystem shrinks.

In this reverse flywheel state, the price of $BERA, the TVL of the ecological protocol, and the overall profit of the ecosystem will decrease until the conditions for flywheel operation are met again.

If we only consider the demand within the ecosystem in the near future, 1) it is expected that there will be many protocols seeking to issue their own tokens as rewards; 2) since the emission of $BGT has just started, the farming efficiency of each $BGT is very high, so the demand for providing liquidity and accumulating $BGT will be relatively high。

For these reasons, Flywheel is likely to operate in the early stages of the mainnet launch, but factors such as macro markets and investment trends in other industries will also affect the operation of Flywheel, so it is difficult to say whether Flywheel will operate successfully.

Next, we will explore several risk factors and scenarios that may trigger the reverse flywheel during the period of flywheel operation.

3. Reverse flywheel plot

3.1. $BERA crash

$BERA plays the following key roles in the Berachain ecosystem:

- Staking for running a node

- Guaranteed minimum value of $BGT

- Used as a deposit asset in various liquidity pools

Therefore, the downward trend in the value of $BERA can also be seen as a weakening of network security, a decrease in the minimum value of $BGT, and a decrease in ecological liquidity. For participants in the Berachain network, the price of $BERA plays a more important role than the price of mainnet tokens for participants in other networks.

When the flywheel is running smoothly, even if the price of $BERA falls to some extent, demand for $BERA can continue to be created if the incentive yield is maintained. But on the contrary, the decline in the value of $BERA may have a negative impact on the ecological protocol, reducing the incentive yield, causing users’ demand to burn $BGT to exchange for $BERA, or to remove the $BERA supplied to the liquidity pool and sell it on the market. This could be the start of a reverse flywheel, causing the value of $BERA to drop again.

Therefore, we should pay special attention to the following situations:

3.1.1. Large-Scale $BERA Unlocking

In addition to $BERA issued through $BGT burning, there is also a planned $BERA unlocking plan, with a total issuance amount of 500M, and the unlocking schedule is as follows:

$BERA Unlock Schedule; Source: Berachain Docs

The linear unlocking plan for investors, early core contributors, and independent community allocations will begin in February 2026, one year after the launch of the mainnet. Prior to this, factors that may trigger selling pressure in the market due to increased $BERA liquidity in the short term include:

- Allocations received by the protocol and community through the RFB program (approximately 2.04% of total issuance)

- Quotations to be allocated through the Boyco program (approximately 2% of total issuance)

Among them, the amount distributed by the protocol and the community to users through the RFB program must have a distribution period of at least 6 months, and since the distribution time of each protocol will be different, it is not expected to cause significant selling pressure on the market in a short period of time.

However, Boyco’s distribution amount is expected to be distributed in approximately 2 months, in a manner similar to current airdrops. In this case, $BERA equivalent to approximately 2% of the total issuance would be supplied to the market, potentially causing selling pressure. In addition, assets deposited in the Boyco plan will also be unlocked when the $BERA airdrop is distributed, which may lead to a reduction in liquidity within the ecosystem. This will create a favorable environment to trigger a reverse flywheel, causing $BERA price and ecological liquidity to decline simultaneously.

Therefore, it will be important to see whether Eco can establish an attractive flywheel before the end of the Boyco plan to effectively absorb the liquidity of $BERA and Eco released into the market.

3.1.2. Mass exit and panic selling of $BGT holders

To earn $BGT, users must deposit liquidity into a liquidity pool capable of issuing BGT rewards and invest sufficient time. However, by BeraHub of Redeem Function, users can burn the $BGT delegated to the validator at any time and obtain $BERA for sale, which only takes about 5 hours to unlock.

Berachain requires an Unboost time of about 5 hours; Source: BeraHub

If users who hold a large amount of $BGT exit the ecosystem at the same time, the circulation of $BERA may increase rapidly. If the price of $BERA drops sharply in a short period of time, it may induce panic selling by other $BGT holders and users who provide $BERA liquidity, leading to a larger decline. Therefore, it is necessary to monitor the burn volume trend of $BGT to understand the dynamics of the current ecosystem.

$BGT Emission & Burn Trend; Source: @thj

Additionally, the reward rate and $BGT yield trends by providing liquidity are the most critical factors in determining $BGT burning and delegation demand. By continuing to observe each trend, it is possible to predict, to a certain extent, the potential risk scenarios that trigger the above mentioned, as well as the likelihood of flywheel recovery if a massive $BGT burn occurs.

At the same time, the demand for liquid $BGT tokens will increase as the incentive rate increases, causing the price to rise; and as the incentive rate decreases, the demand will decrease, and the price will decrease. Therefore, if it is difficult to obtain data on past reward rates and $BGT yields, its approximate value can be estimated by the premium trend of liquid $BGT relative to $BERA, which reflects the intrinsic value of $BGT.

iBGT/B

ERA Price Chart; Source: Dex Screener

However, the price of liquid $BGT tokens is affected not only by the intrinsic value of $BGT, but also by how incentives are distributed in the liquidity protocol and protocol-related factors, so these factors should also be considered together.

3.2. Slowing inflation and growth

In addition to the 500M $BERA distributed to network participants within three years of mainnet launch, Berachain has an annual inflation rate of $BGT of approximately 10%. Although some of the network fees submitted by users will be burned, since Berachain’s main activity is to deposit assets into liquidity pools and collect interest, it is difficult to expect a significant amount to be burned.

This means that even if Berachain establishes a positive flywheel three years from now when all $BERA is unlocked, to sustain it for a year would require a way to attract inflows of external funds that are greater than the inflation rate during that period.

Founder of Berachain Smokey The Bera Accepting Bell Curve interviewmentioned that they are developing a dynamic inflation model that changes based on the reward rate for distributing $BGT to make up for the above issues.

While this feature may help control the acceleration of the flywheel and contribute to the sustainability of development, as long as “inflation” persists, the reverse flywheel leading to the price decline of $BERA and ecological contraction is inevitable at a certain stage. Therefore, even from a long-term perspective, several ecological indicators mentioned above must be continuously monitored to diagnose the current status of the ecology.

In addition, in Berachain, the strategy of simply holding $BERA spot for a long time without utilizing it in the ecosystem is an inefficient investment method and will not be able to recover the value diluted due to “inflation”. Therefore, for users who want to take advantage of $BERA to open a position, depositing it into the ecological protocol to actively generate interest is a very important strategy.

If users want to establish a stable position in the ecosystem for a long time, conservatively using assets less affected by flywheel prices (such as $BTC, $ETH, stablecoins, etc.) to accumulate $BGT or perform double-entry deposit operations may be an effective method.

3.3. Monopoly $BGT

In the PoS structure used by most recently launched mainnets, entities with larger stakes receive greater network rewards. This leads to the consolidation of validator stakes and poses a risk of network centralization.

Validator Staking Market Share in the Ethereum Network; Source: @hildobby

Berachain, which was created by modifying the basic PoS structure, also experienced this phenomenon. In addition, in Berachain, validators holding a large amount of $BGT can directly intervene in the ecosystem and unilaterally design a structure that is beneficial to themselves. Therefore, $BGT monopoly will lead to ecological monopoly. Compared with other PoS-based networks, there will be a greater risk of network token monopoly.

To prevent this problem, the team capped $BERA staking that affects block creation authority to 10M and introduced a method where Boosting inefficiently increases as the amount of $BGT representation that determines the $BGT generated per block increases. However, these limitations can be circumvented by operating multiple nodes distributed by a single entity, or through collusion between multiple validators.

In particular, the Liquidized $BGT protocol has an advantage in attracting liquidity for use in the Berachain Reward Vault, as the potential value of “liquidity” is high and can directly accumulate $BGT on behalf of users by depositing liquidity received from users into the Reward Vault. In addition, by awarding this $BGT back to the nodes they operate or cooperate with, this kind of agreement can obtain a large amount of $BGT emission voting rights without negotiating with other ecological entities.

If these protocols discharge additional $BGT of these voting rights into a liquidity pool containing liquidized $BGT tokens, the liquidized $BGT protocol can set up its own independent flywheel, increasing demand for the liquidity provided to the protocol without even having to pay independent rewards.

In this case, the flywheel of liquifying the $BGT protocol itself becomes as powerful as the ratio of $BGT held by the protocol to the total $BGT issued within the ecosystem. If multiple liquid $BGT protocols obtain a large amount of $BGT in the above-mentioned manner and continue to pursue the direction of only increasing the liquidity supply demand of their own liquid $BGT tokens, it may inhibit the liquidity improvement of other protocols and hinder the launch and development of new protocols, thus limiting the diversity of the ecosystem, ultimately causing the ecological scale to shrink and triggering a reverse flywheel.

As mentioned before, the $BGT monopoly can be structurally restricted through the protocol operating mechanism, but it is difficult to completely block it. Therefore, the most certain way to prevent specific entities from monopolizing the ecology is for participants to reach a consensus on ecological sustainability before the monopoly structure is consolidated, and to continue paying attention and working hard for this consensus in the community.

4. Summary

So far, we have explored how Berachain’s flywheel works, the conditions under which it operates, and the reverse flywheel plot. In addition to the possibilities introduced in this article, the reverse flywheel will also operate if the three conditions for driving the flywheel cannot be met, so it is very important to continue to pay attention to network and ecological indicators to evaluate the operating status of the flywheel in Berachain.

Additionally, unfamiliar PoL mechanisms and the various forms of DeFi protocols that exploit them are combining to create complex derivatives and synthetic assets that are difficult to intuitively understand. Therefore, users need to proactively understand their position structure and be aware of overlapping structural and security risks in advance.

From a long-term perspective, the challenge Berachain faces is to continue to expand the ecosystem while also formulating a strategy to increase network fees to cope with the possibility of a reverse flywheel caused by inflation. It is necessary to pay close attention to whether consumer applications such as Perp DEX or on-chain games can settle in the ecosystem to generate real user traffic beyond “simple deposits”.

I hope this article can clearly help users understand the Berachain ecosystem and effectively respond when the reverse flywheel comes.

Disclaimer:

- This article is reproduced from [DeSpread], and the copyright belongs to the original author [Tranks], if you have any objection to the reprint, please contact Gate Learn team, the team will handle it as soon as possible according to relevant procedures.

- Disclaimer: The views and opinions expressed in this article represent only the author’s personal views and do not constitute any investment advice.

- Other language versions of the article are translated by the Gate Learn team and are not mentioned in Gate.io, the translated article may not be reproduced, distributed or plagiarized.

บทความที่เกี่ยวข้อง

In-depth Explanation of Yala: Building a Modular DeFi Yield Aggregator with $YU Stablecoin as a Medium

What is Stablecoin?