Is Solana’s DeFi Undervalued? The Battle Between High-Yield Staking and Struggling Lending Protocols

Recently, the traditional financial giant Franklin Templeton released a research report on the Solana DeFi ecosystem, stating that although Solana’s DeFi sector has far outpaced Ethereum in terms of transaction volume growth and protocol revenue, its associated tokens remain severely undervalued. Data shows that in 2024, Solana’s leading DeFi projects had an average growth rate of 2,446% (compared to Ethereum’s 150%), while its market cap-to-revenue ratio was only 4.6x (Ethereum’s was 18.1x), making it appear as a value investment opportunity by comparison.

However, while the market marvels at Solana DEXs dominating 53% of global trading volume, another side of the ecosystem is experiencing turbulence. Following the MEME coin frenzy, on-chain trading volume plummeted by over 90%. Meanwhile, validator nodes offering staking yields of 7%-8% act as a black hole sucking up liquidity, leaving lending protocols struggling under yield compression. This valuation paradox has triggered a reassessment of Solana’s DeFi landscape, bringing it to a critical crossroads—should it continue to position itself as the “Crypto Nasdaq”, or should it take the riskier path of transforming into a full-spectrum financial protocol battleground? The upcoming vote on SIMD-0228, a proposal to reduce inflation, may determine the final direction of this ecosystem revolution.

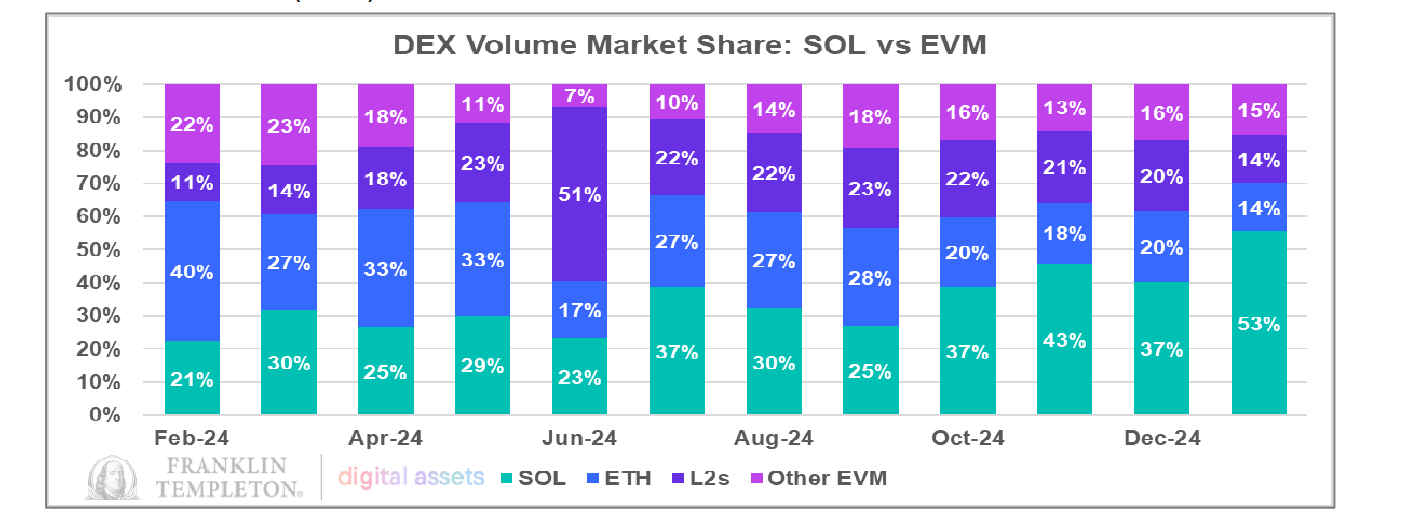

Solana DEX Trading Volume Now Accounts for Half of the Market

Franklin Templeton’s report primarily builds its argument around Solana’s DEX market share. In fact, over the past year, Solana’s DEX trading volume has indeed achieved impressive milestones.

In January, Solana’s DEX trading volume surpassed not only Ethereum’s DEX volume but also the combined trading volume of all Ethereum Virtual Machine (EVM)-based DEXs, reaching 53% of the total market share.

A comparison of top DeFi projects on Solana and Ethereum further highlights this trend. In 2024, the top five DeFi projects on Solana recorded an average growth rate of 2,446%, while Ethereum’s top DeFi projects grew by only 150%. In terms of market cap-to-revenue ratio, Ethereum’s average stands at 18.1x, whereas Solana’s is just 4.6x. From this perspective, Solana’s DeFi projects appear to have an advantage in revenue and trading volume. However, does this necessarily mean that Solana DeFi is undervalued? And can DeFi growth on Solana become the dominant trend moving forward? To answer these questions, a deeper understanding of the unique ecosystem characteristics of both networks is required.

Choosing an Ecosystem Identity: Trading Hub or Universal Bank?

A comparison of Ethereum and Solana’s DeFi protocols reveals a stark contrast: on Ethereum, the top five DeFi projects are predominantly staking and lending-focused.

On Solana, however, the top five TVL-ranked projects are mostly aggregators or DEXs, making trading the dominant theme on the network.

From this perspective, if both ecosystems were compared to financial institutions, Ethereum would resemble a bank, while Solana would be more akin to a securities trading center. One specializes in credit-based financial services, while the other is focused on trading, highlighting their fundamental differences in positioning.

However, both networks now face significant challenges. Ethereum, which relies heavily on credit-based protocols, struggles with value retention. Meanwhile, Solana, which thrives on trading activity, is experiencing a sharp decline in market liquidity.

To address this imbalance, expanding Solana’s lending sector might be a viable strategy. However, such a transition will be long and difficult. Since January, Solana’s TVL has dropped by 40%, though this decline is largely due to SOL’s price drop, rather than a significant outflow of funds from the network.

Since Trump launched his personal token, Solana’s DEX trading volume has been in a continuous downtrend. On January 18, DEX trading volume hit an all-time high of $35 billion, but by March 7, it had plummeted to just $2 billion.

After the MEME Frenzy Fades, Capital Competes for Staking Yields

In contrast to declining SOL prices and the cooling of the MEME coin market, the number of staked tokens on-chain has actually continued to rise in recent weeks. Take Jito, the top-ranked protocol by TVL, for example—its staked SOL volume has been consistently increasing, reaching 16.47 million SOL. Looking at capital inflows, Jito has maintained a net inflow of tokens in recent weeks. Since January 1, 2025, SOL’s net staking inflows have grown 12% year-over-year. Clearly, this TVL growth is driven primarily by staking rather than trading activity.

However, this asset growth has not flowed into lending protocols—instead, it has continued to concentrate in validator staking rewards. Even though staking yields for validators have been declining, they still attract the majority of SOL’s TVL.

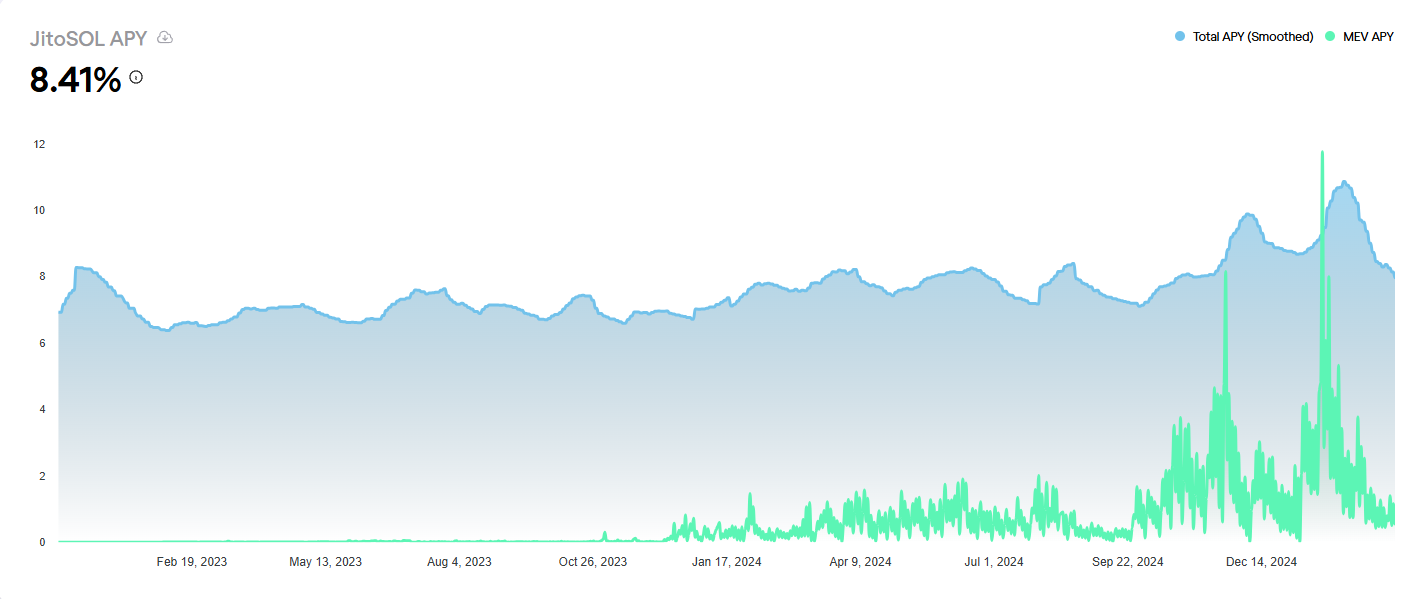

According to Jito’s data, since February, JitoSOL’s APY has been in a continuous downtrend, mirroring the decline in bundled transactions and priority fee revenues across the network. As of March 7, JitoSOL’s APY has dropped to 8.41%. However, it still remains at least 3 percentage points higher than other staking yield options on Kamino.

8% Validator Yields Suppress DeFi Liquidity, SIMD-0228 Proposal Aims to Break the Deadlock

On Solana, validator staking yields have remained around 7%-8%, consistently higher than returns from most other DeFi protocols. This explains why a large portion of capital on Solana prefers to stake with validators rather than participating in lending protocols like Kamino.

Recently, Solana introduced the SIMD-0228 proposal, which aims to dynamically adjust inflation rates by reducing SOL’s annual issuance by 80%. At the same time, it plans to lower staking yields, encouraging capital to flow into other DeFi sectors. (Related reading: Solana Inflation Revolution: The SIMD-0228 Proposal Sparks Community Controversy-Hidden “Death Spiral” Risk Behind the 80% Issuance Cut).

According to simulations based on the proposal, staking yields would drop to 1.41%, marking an 80% decline in returns if staking volumes remain unchanged. As a result, a majority of capital may exit validator staking, shifting toward higher-yielding DeFi products.

However, there is a logical flaw in this approach—the best way to incentivize capital movement into DeFi should be enhancing yields on DeFi protocols, rather than reducing staking rewards. When capital exits validator staking, it is not guaranteed to stay within the Solana ecosystem. Given capital’s natural pursuit of higher yields, it is more likely to flow toward better opportunities elsewhere.

A comparison with Ethereum’s largest TVL projects, such as Aave and Lido, shows that mainstream asset yields range between 1.5%-3.7% APY. In contrast, Solana’s Kamino still holds a yield advantage.

However, for large-scale capital, another crucial factor is liquidity depth. Ethereum remains the largest liquidity hub among all blockchains—as of March 7, Ethereum’s TVL still accounts for 52% of the total market, dominating half of the industry. Meanwhile, Solana holds a TVL share of just 7.53%. The largest TVL project on Solana, Jito, has $2.32 billion in TVL, which would only rank 13th within Ethereum’s ecosystem.

At present, Solana DeFi still relies on high yields to attract liquidity. For example, SVM and the re-staking platform Solayer recently launched native SOL staking, offering a direct yield of approximately 12%. However, PANews’ analysis suggests that these high yields are still primarily derived from validator staking strategies.

If SIMD-0228 is implemented, DeFi protocols that depend on validator staking rewards may face a liquidity exodus and potential liquidation risks. After all, many high-yield products are fundamentally reliant on validator staking revenues.

In the evolution of Solana’s DeFi ecosystem, while its DEX trading volume briefly reached the top, proving the explosive potential of its technical architecture, the inverse relationship between staking yields and DeFi growth hangs over the ecosystem like the Sword of Damocles. The SIMD-0228 proposal aims to cut this Gordian knot, but a forced reset of staking yields could trigger a more complex on-chain butterfly effect than expected. Solana Foundation Chair Lily Liu also expressed concerns about the proposal on X, stating that “SIMD-0228 is too unfinished” and could introduce greater uncertainty.

From a long-term strategic perspective, Solana needs more than just a realignment of yield curves—it requires a fundamental overhaul of its value capture mechanism. Only when validator staking shifts from being a yield fortress to a liquidity hub, or when lending protocols develop yield strategies that go beyond simple staking, can Solana truly complete its DeFi value loop. After all, true ecosystem prosperity doesn’t come from stacking numbers in staking pools, but from capital flowing continuously through lending, derivatives, and composable strategies—a perpetual motion cycle that may be the ultimate “Goldbach conjecture” for Ethereum killers to solve.

Disclaimer:

This article is reposted from [PANews]. Copyright belongs to the original author [Frank, PANews]. If there are any concerns regarding this republication, please contact the Gate Learn team, and the team will handle the matter promptly according to the relevant process.

Disclaimer: The views and opinions expressed in this article represent only the author’s personal views and do not constitute any investment advice.

Other language versions of this article have been translated by the Gate Learn team. Unless explicitly credited to Gate.com, translated versions may not be copied, distributed, or reproduced.

Share

Content

Related Articles

The Future of Cross-Chain Bridges: Full-Chain Interoperability Becomes Inevitable, Liquidity Bridges Will Decline

Solana Need L2s And Appchains?

Sui: How are users leveraging its speed, security, & scalability?

Navigating the Zero Knowledge Landscape

What is Tronscan and How Can You Use it in 2025?