When Slow Assets Meet Fast Markets

Introduction

The slowest assets in finance—loans, buildings, commodities—are being strapped onto the fastest markets in history. Tokenization promises liquidity, but what it really creates is an illusion: a liquid shell wrapped around an illiquid core. That mismatch is the RWA Liquidity Paradox.

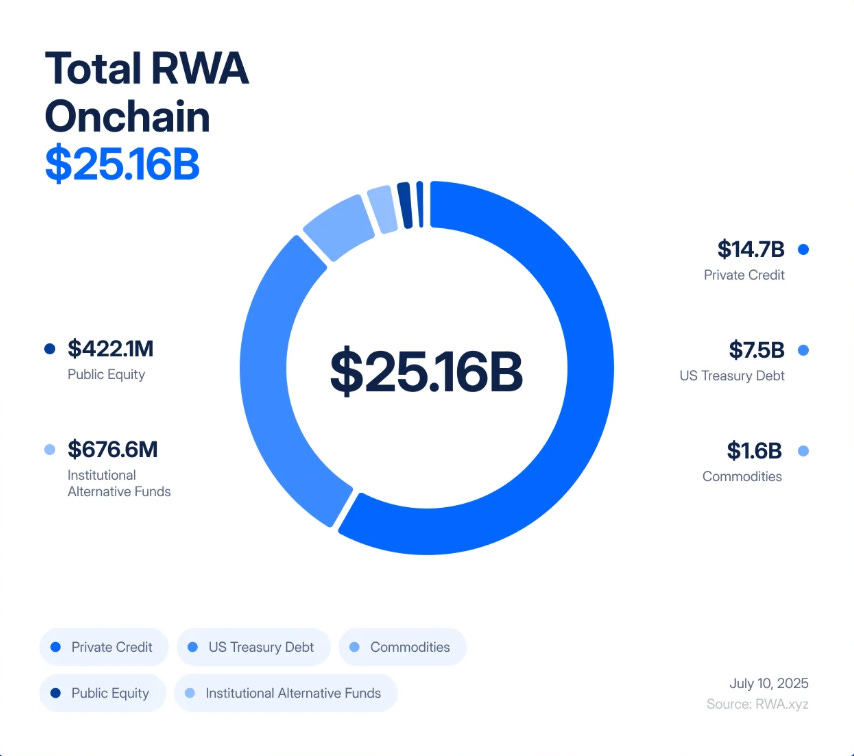

In just five years, tokenized real-world assets (RWAs) have surged from an $85 million experiment to a $25 billion market, growing by “245x during 2020-2025, driven by institutional demand for yield, transparency, and balance sheet efficiency”.

BlackRock issues tokenized Treasuries, Figure Technologies has put billions in private credit on-chain, and real estate deals from New Jersey to Dubai are being fractionalized and traded on decentralized exchanges.

Analysts project trillions of dollars of assets could soon follow. To many, this looks like the long-awaited bridge between TradFi and DeFi—a chance to finally merge the safety of real-world yield with the speed and transparency of blockchain rails.

But beneath the enthusiasm lies a structural flaw. Tokenization doesn’t change the fundamental nature of an office building, a private loan, or a gold bar. These are slow, illiquid assets—legally and operationally bound by contracts, registries, and courts. What tokenization does is wrap them in hyper-liquid shells that can be traded, leveraged, and liquidated instantly. The result is a financial system where slow-moving credit and valuation risks are converted into high-frequency volatility risks, with contagion that spreads not over months but minutes.

If this sounds familiar, it should. In 2008, Wall Street discovered the hard way what happens when illiquid assets are transformed into “liquid” derivatives. Subprime mortgages collapsed slowly; Collateralized Debt Obligations (CDOs) and Credit Default Swaps (CDS) collapsed quickly. The mismatch between real-world defaults and financial engineering detonated the global system. The danger today is that we are recreating this architecture—only now it runs on blockchain rails, where crisis moves at code-speed.

Imagine a token tied to a commercial property in Bergen County, New Jersey. On paper, the building is solid: tenants pay rent, the mortgage is serviced, the deed is clear. But the legal process to transfer that deed—title checks, signatures, filings with the county clerk—takes weeks. That’s how real estate works: slow, methodical, bound by paper and courts.

Now put that same property on-chain. The deed sits inside a Special Purpose Vehicle, which issues digital tokens representing fractional ownership. Suddenly, what was once a sleepy asset can be traded 24/7. In a single afternoon, those tokens might change hands hundreds of times on decentralized exchanges, collateralize stablecoins in lending protocols, or be bundled into structured products promising “safe, real-world yield.”

Here’s the catch: nothing about the building itself has changed. If a major tenant defaults, if property values slide, if the SPV’s legal claim is challenged, the real-world impact unfolds over months or years. But on-chain, confidence can evaporate instantly. A rumor on Twitter, a delayed oracle update, or a sudden sell-off is enough to trigger a cascade of automated liquidations. The building doesn’t move, but the tokenized representation of it can collapse in minutes—dragging collateral pools, lending protocols, stablecoins, all down with it.

This is the essence of the RWA Liquidity Paradox: the illusion that strapping illiquid assets onto hyper-liquid markets makes them safer, when in fact it makes them more explosive.

2008 in Slow Motion vs. 2025 in Real Time

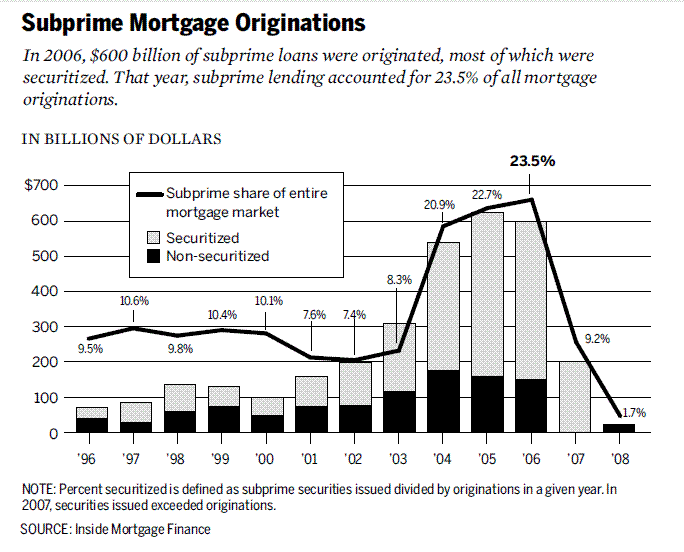

In the mid-2000s, Wall Street turned subprime mortgages—illiquid, risky loans—into complex securities.

Mortgages were pooled into Mortgage-Backed Securities (MBS), then sliced into tranches as Collateralized Debt Obligations (CDOs). To hedge, banks layered on Credit Default Swaps (CDS). On paper, this alchemy created “safe” AAA assets from fragile subprime loans. In practice, it built a tower of leverage and opacity on a shaky foundation.

The crisis came when the slow drip of mortgage defaults collided with the fast-moving world of CDOs and CDS. Houses took months to foreclose, but the derivatives tied to them repriced in seconds. That mismatch didn’t cause the collapse alone—but it amplified it from local defaults into a global shock.

RWA tokenization risks replaying this same mismatch—only faster. Instead of tranching subprime mortgages, we’re fractionalizing private credit, real estate, and Treasuries into on-chain tokens. Instead of CDS, we’ll see “RWA-squared” derivatives: options, synthetics, and structured products on top of RWA tokens. And instead of rating agencies stamping junk with AAA, we now outsource valuation to oracles and custodians—new black boxes of trust.

The parallel is not superficial. The very logic is the same: take illiquid, slow assets; wrap them in structures that appear liquid; and let them circulate in markets that move orders of magnitude faster than the underlying. In 2008, the system collapsed in months. In DeFi, contagion would spread in minutes.

Scenario 1: The Credit Default Cascade

A private credit protocol has tokenized $5B worth of SME loans. On paper, the yields are steady—8 to 12%. Investors treat the token as safe collateral, borrowing against it on Aave and Compound.

Then the real economy turns. Defaults tick up. The true value of the loan book falls, but the oracle feeding on-chain prices only updates monthly. On-chain, the token still looks sound.

Whispers spread: a few big borrowers missed payments. Traders rush to sell before the oracle catches up. The market price of the token slips below its “official” value, breaking the peg.

That’s enough to trigger the machines. DeFi lending protocols register the falling price and automatically liquidate loans backed by the token. Liquidator bots repay debts, seize the collateral, and dump it on exchanges—pushing the price even lower. More liquidations fire. In minutes, a feedback loop turns a slow credit problem into a full-blown on-chain crash.

Scenario 2: The Real Estate Flash Crash

A custodian overseeing $2B of tokenized commercial properties suffers a hack and admits its legal claims on the deeds may be compromised. At the same time, a hurricane hits a city where many of the buildings sit.

The off-chain value of the assets is in doubt; the on-chain tokens collapse immediately.

On decentralized exchanges, panicked holders stampede for the exit. Automated Market Makers are drained of liquidity. The token’s price goes into free-fall.

Across DeFi, that token had been pledged as collateral. Liquidations fire, but the seized collateral is worthless and illiquid. Lending protocols are left with unrecoverable bad debt. What was marketed as “institutional grade real estate on-chain” becomes an instant hole in the balance sheets of DeFi protocols—and any TradFi funds exposed to them.

Both scenarios show the same dynamic: the liquidity shell collapses faster than the underlying asset can respond. The building still stands. The loan still exists. But on-chain, the representation evaporates in minutes, dragging the rest of the system with it.

The Next Phase: RWA-Squared

Finance never stops at the first layer. Once an asset class exists, Wall Street (and now DeFi) builds derivatives on top of it. Subprime mortgages gave us Mortgage-Backed Securities, then CDOs, then CDS. Each layer promised better risk management; each layer amplified fragility.

RWA tokenization will be no different. The first wave is straightforward: fractionalized credit, Treasuries, real estate. The second wave is inevitable: RWA-squared. Tokens bundled into indices, tranches carved into “safe” and “risky” slices, synthetics that let traders bet on or against baskets of tokenized loans or properties. A token backed by real estate in New Jersey and SME loans in Singapore can be repackaged into a single “yield product” and leveraged across DeFi.

The irony is that on-chain derivatives will look safer than 2008’s CDS because they’re fully collateralized and transparent. But the risks won’t vanish—they’ll mutate. Smart contract bugs replace counterparty defaults. Oracle errors replace ratings fraud. Protocol governance failures replace AIG. The outcome is the same: layers of leverage, hidden correlations, and a system vulnerable to a single point of failure.

The promise of diversification—mixing Treasuries, credit, and real estate in a tokenized basket—ignores the reality that all those assets now share one correlation vector: the DeFi rails themselves. A failure in a major oracle, stablecoin, or lending protocol would crash every RWA derivative built on top, no matter how diverse the underlying assets.

RWA-squared products will be marketed as the bridge to maturity, the proof that DeFi can recreate sophisticated TradFi markets. But they may also be the accelerant that ensures when the first shock comes, the system doesn’t bend—it breaks.

Conclusion

The RWA boom is being sold as the great bridge between traditional and decentralized finance. Tokenization does bring efficiency, composability, and new access to yield. But it does not change the nature of the assets themselves: loans, buildings, and commodities remain slow and illiquid, even when their digital wrappers trade at blockchain speed.

That is the Liquidity Paradox. By strapping illiquid assets onto hyper-liquid markets, we increase fragility and reflexivity. The same tools that make markets faster and more transparent also make them more exposed to sudden shocks.

In 2008, it took months for subprime defaults to metastasize into a global crisis. With tokenized RWAs, a similar mismatch could transmit in minutes. The lesson isn’t to abandon tokenization, but to design with its risks in mind: more conservative oracles, better collateral standards, and stronger circuit breakers.

We are not condemned to repeat the last crisis. But if we ignore the paradox, we may end up accelerating it.

Disclaimer:

- This article is reprinted from [Tristero Research]. All copyrights belong to the original author [Tristero Research]. If there are objections to this reprint, please contact the Gate Learn team, and they will handle it promptly.

- Liability Disclaimer: The views and opinions expressed in this article are solely those of the author and do not constitute any investment advice.

- Translations of the article into other languages are done by the Gate Learn team. Unless mentioned, copying, distributing, or plagiarizing the translated articles is prohibited.

Share

Content

Related Articles

Reshaping Web3 Community Reward Models with RWA Yields

ONDO, a Project Favored by BlackRock

What is Plume Network

What Are Crypto Narratives? Top Narratives for 2025 (UPDATED)

Real World Assets - All assets will move on-chain