Bitcoin monthly options will expire on March 27 (Friday) at 8:00 AM UTC, with open interest totaling $18.6 billion. Call options (buy) dominate in nominal terms, amounting to $11.2 billion, while put options (sell) are $7.4 billion. If Bitcoin remains around $70,900 by Friday’s expiry, up to 92% of open call options will expire worthless.

Call options lead in nominal value, but the actual advantage is nearly zero

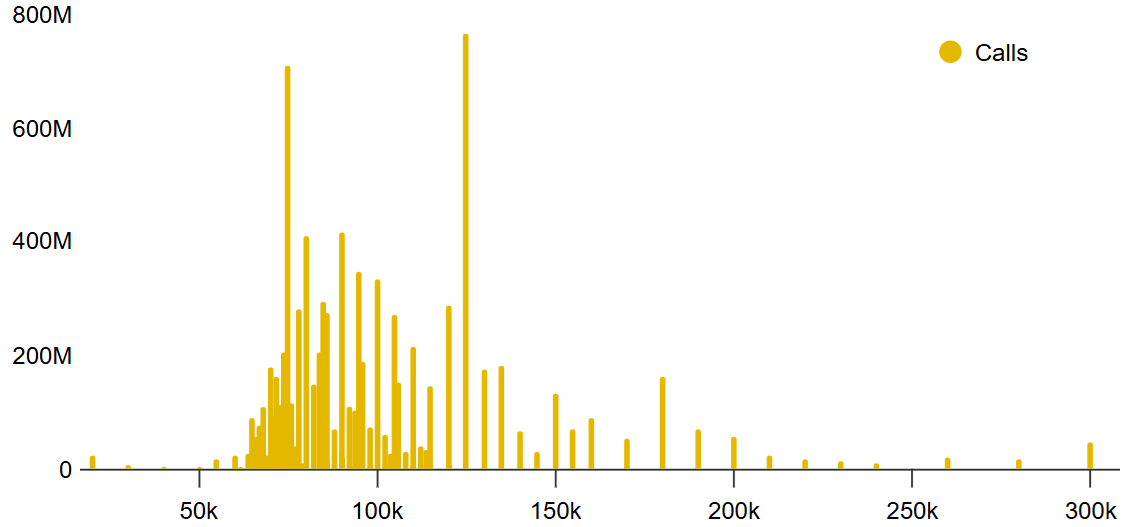

(Source: Deribit)

(Source: Deribit)

Deribit dominates this expiry with a 76% market share, with open interest reaching $14.1 billion, followed by OKX (7.1%) and CME (6.6%). Looking at Deribit’s call options distribution, long positions are heavily concentrated at strike prices of $90,000 and above—most of these positions were established when Bitcoin traded over $86,000 in February, before traders expected the quarterly expiry price to fall back near $71,000.

Currently, Deribit’s call options with strike prices below $78,000 amount to only about $2 billion, meaning that at current levels, 77% of call options could expire worthless on Friday; if Bitcoin stays at $71,000, the expiry rate would rise to 92%. On the put side, open interest at strikes of $66,000 and above totals $2.2 billion, with 40% expiring on Friday, indicating a clear structural advantage for bears at current price levels.

Four settlement scenarios: key price levels determining bulls vs. bears

Based on Deribit’s open interest distribution, four key scenarios exist for Friday’s expiry:

$65,000 to $69,000: Net outcome favors bears, with puts gaining about $1.8 billion

$69,001 to $72,000: Bears still hold the advantage, with puts gaining about $950 million

$72,001 to $75,000: Puts continue to lead, but gains shrink to around $430 million

$75,001 to $78,000: Bulls turn the tide, with calls gaining about $790 million

In the first three scenarios, bears have the advantage. The effective reversal point for bulls is clearly above $75,001, requiring an increase of over 6% from current levels.

Macro triple pressure: inflation, geopolitical conflicts, and credit tightening

(Source: TradingView)

(Source: TradingView)

The bearish structural advantage is not only technical; macro headwinds reinforce traders’ confidence in short positions. WTI crude remains above $90, keeping inflation pressures high, which dampens expectations of the Fed easing. The ongoing Israel-Iran conflict, involving U.S. intervention, adds geopolitical uncertainty, prompting traders to avoid risk assets.

A third layer of pressure comes from the $3 trillion private credit market. According to CNBC, asset managers like Ares Management, Apollo Global Management, Blue Owl Capital, and Cliffwater have been forced to pause or limit redemptions, signaling early signs of deteriorating credit quality. If liquidity in the private credit market continues to tighten, it could further reduce overall risk appetite. Bitcoin has fluctuated within a narrow range of $67,700 to $71,600 over the past week, with S&P 500 futures moving in sync with Bitcoin, indicating the crypto market is still following overall macro sentiment.

FAQs

Q: How does this Bitcoin options expiry affect the spot market?

Options expiry itself doesn’t directly impact the spot market, but price movements near the “max pain” point can trigger market participants to adjust hedges, indirectly influencing short-term price momentum. The $18.6 billion scale is a quarterly large settlement, and market liquidity tends to be more sensitive around expiry.

Q: Why might 92% of call options expire worthless on Friday?

Many long positions were established when Bitcoin traded over $86,000 in February, mainly at strike prices above $90,000. As the price drops toward $71,000, these options are deep out-of-the-money. On Deribit, call options with strikes below $78,000 total only about $2 billion, leaving very limited effective protection for longs.

Q: What are the main macro downside risks for Bitcoin currently?

Three primary risks: sustained high WTI crude prices maintaining inflation pressures; escalating geopolitical conflicts involving the U.S., Israel, and Iran increasing risk aversion; and the $3 trillion private credit market seeing multiple institutions restrict redemptions, highlighting potential deterioration in credit conditions. These factors collectively suppress Bitcoin’s short-term upside potential.

Disclaimer: The information on this page may come from third parties and does not represent the views or opinions of Gate. The content displayed on this page is for reference only and does not constitute any financial, investment, or legal advice. Gate does not guarantee the accuracy or completeness of the information and shall not be liable for any losses arising from the use of this information. Virtual asset investments carry high risks and are subject to significant price volatility. You may lose all of your invested principal. Please fully understand the relevant risks and make prudent decisions based on your own financial situation and risk tolerance. For details, please refer to

Disclaimer.