The Executive Yuan has approved the draft “Virtual Asset Services Act,” which will regulate service providers into 7 categories and adopt a licensing-and-permit system. The new law will tightly control asset custody and explicitly ban stablecoins from paying interest. If the matter involves fraud, the maximum penalty will be NT$200 million; with that, Taiwan’s crypto industry is set to enter a compliant era.

- This article was updated and revised on 2026/4/8 to the version approved by the Executive Yuan

The draft Virtual Asset Services Act has passed the Executive Yuan—easy-to-follow rundown in one go

Taiwan’s cryptocurrency industry has finally entered a clear regulatory era! Following the Financial Supervisory Commission’s release of a preliminary draft last year, the Executive Yuan has approved the amendments to the “Virtual Asset Services Act” in early April this year and will submit it to the Legislative Yuan for review. The goal is to improve the development and management of Taiwan’s virtual asset businesses, protect the rights and interests of traders, and promote financial technology innovation.

Compared with the 2025 version, the Executive Yuan’s approved version is stricter in both penalties and management! After reading through the complex legal provisions, Crypto City laid out four key points to help readers quickly understand them. If you want the latest full draft text, you can check this “Virtual Asset Services Act” PDF file.

Four key points of the draft Virtual Asset Services Act

Key point 1: Classification of virtual asset service providers and license application

The draft “Virtual Asset Services Act” clearly stipulates that virtual asset service providers must obtain the necessary permits from the competent authority according to their respective categories, and only after receiving the license permit (license) may they operate. Virtual asset businesses may not be operated without permission and the issuance of the license permit.

In addition, the revised draft explicitly states that “businesses may not operate unless they join the industry association,” implementing industry self-discipline. After obtaining permission, traditional financial institutions may also “engage in” virtual asset-related business, and are exempt from certain requirements.

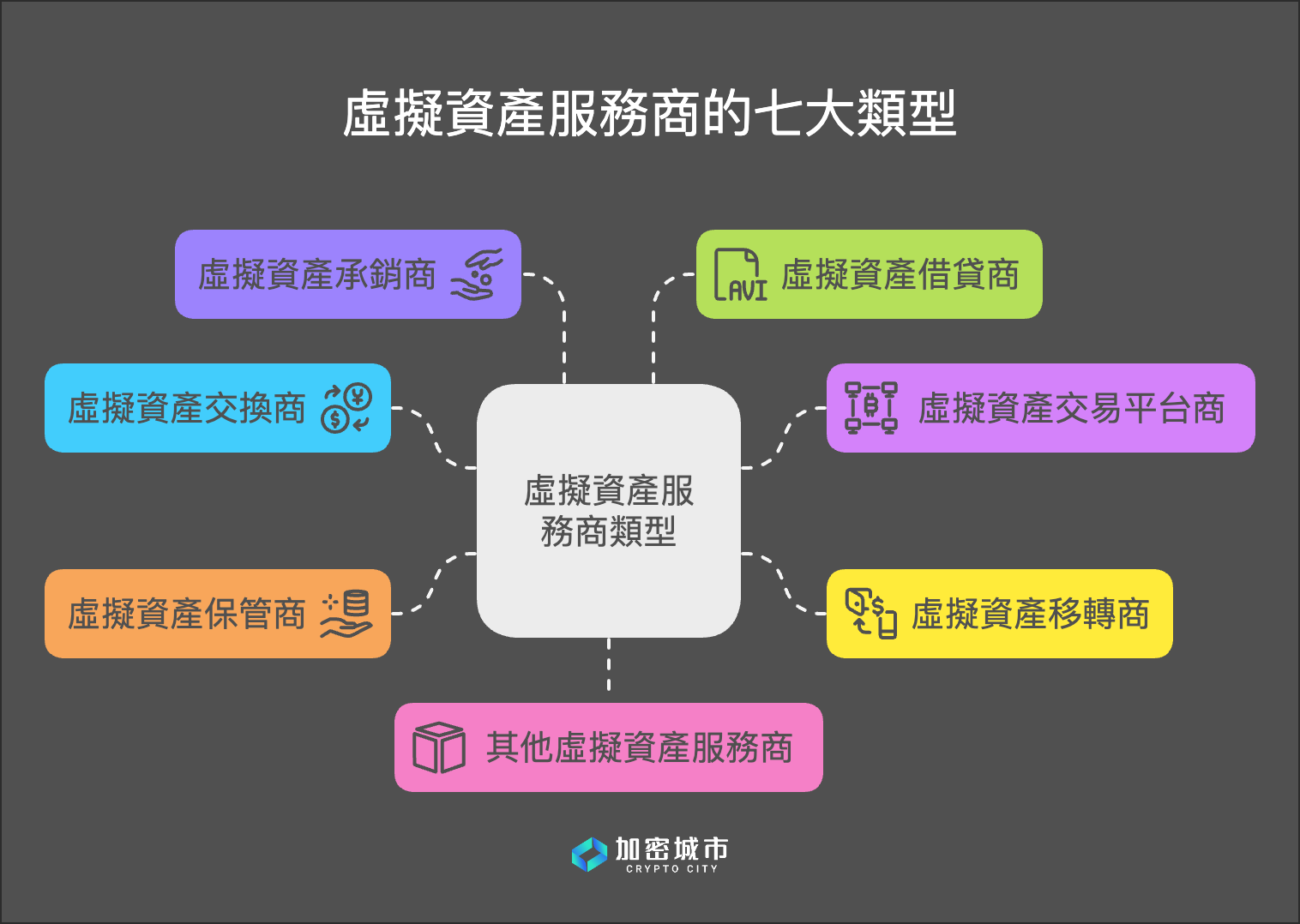

The Financial Supervisory Commission will categorize virtual asset service providers into 7 types:

- Virtual asset exchange businesses: Operate the exchange of virtual assets with New Taiwan dollars, foreign currencies, and currencies issued from Mainland China, Hong Kong, or Macau, along with related services; or operate exchanges between virtual assets and related services.

- Virtual asset trading platform businesses: Operate virtual asset exchange business for a centralized virtual asset trading market.

- Virtual asset transfer businesses: Operate the transfer of virtual assets and related services, including related services for virtual asset payments.

- Virtual asset custody businesses: Operate the custody or management of virtual assets, or tools used to control virtual assets, and related services.

- Virtual asset underwriting businesses: Operate the issuance or sale of virtual assets and related services.

- Virtual asset lending businesses: Acquire virtual assets and agree to return or deliver the same or a greater amount or value of virtual assets and related services.

- Other virtual asset service providers: Operate other virtual asset services approved by the competent authority

Image source: Made by Crypto City. Virtual Asset Services Act draft quick guide key points: Types and licenses of virtual asset service providers

License permit (license) application deadline

For the transition period most concerned by businesses, the Executive Yuan’s version includes clearer requirements: businesses that have already completed anti-money-laundering registration must submit an application within 9 months after the law takes effect, and obtain the license permit within 18 months. If they fail to apply by the deadline or fail to pass, they may not continue to operate.

Requirements for foreign currency businesses to land in Taiwan

As for foreign virtual asset service providers (e.g., offshore crypto exchanges), if they want to establish a branch in Taiwan, they must obtain permission from the competent authority and be issued a license permit, and they must register the establishment of a company or branch in Taiwan.

Key point 2: Management framework for virtual asset service providers

The Financial Supervisory Commission also referenced regulations in the EU MiCA and places such as Japan and Singapore, and introduced stringent requirements for virtual asset service providers. Crypto City lists the following key points:

Total liabilities

The total amount of external liabilities of a virtual asset service provider may not exceed the specified multiple(s) of its net worth; its total current liabilities may not exceed the specified percentage of its total current assets. However, this limitation does not apply to entities that are financial institutions and also engage in such business. The competent authority will set the aforementioned multiple(s) and percentage(s).

Internal controls and administrative fines

Service providers must establish internal control systems and cybersecurity requirements. If internal controls are not adequate, if financial reports are not filed as required, or if listing/delisting review is not properly implemented, they will face administrative fines of not less than NT$300,000 and not more than NT$6,000,000, and penalties may be imposed per instance.

Custody of customer assets

Virtual asset service providers must keep assets for customers. These assets must be independently segregated from the provider’s own property in accordance with the methods specified by the competent authority. Customer assets include the customer’s virtual assets, legal tender, and other assets. The creditors of a virtual asset service provider may not make any requests or exercise other rights against the customer assets it holds.

In the event of bankruptcy, customer assets do not form part of its bankruptcy estate (Note). Unless otherwise directed by the customer, offsetting obligations to the extent permitted by law, or with approval by the competent authority, customer assets may not be used. For customer virtual assets held by a virtual asset custody business, the ownership of the property belongs to the customer, and it may not be agreed with the customer that the assets will be transferred. Customer virtual assets may not be mixed and held together with the provider’s own virtual assets.

- Note: “Bankruptcy estate” refers to all assets the company owns before the bankruptcy proceedings are concluded, including movable property, real estate, claims to property, etc., all of which belong to the bankruptcy estate.

Customer legal tender deposit dedicated accounts

A virtual asset service provider may, with the customer’s consent, handle the legal tender retained that is involved in virtual asset business in the same-currency deposit dedicated account opened with a financial institution, and must either deliver the legal tender retained from the customer to a trust or obtain full performance guarantees from the bank. If legal tender retained from customers is involved, the account reconciliation provisions applicable to virtual asset custody businesses will apply.

Periodic review reports

Virtual asset service providers must periodically report to and publish financial reports verified, signed, or reviewed by certified public accountants to the competent authority. The reporting process, items to be published, and formats will be determined by the competent authority.

For the customer assets it holds, a virtual asset custody business must set up recurring reconciliation measures, and appoint certified public accountants to issue reports, and must report to and publish them to the competent authority.

Review of virtual asset listings and delistings

A virtual asset exchange business must publish the offering memorandum (white paper) describing the issuance of the virtual assets for which it provides exchange services. If the virtual assets do not have an offering memorandum prepared and published in accordance with the requirements of the competent authority, then, in principle, the virtual asset exchange business may not provide exchange services for those virtual assets.

A virtual asset trading platform business must set listing/delisting review standards and review procedures. For virtual assets that have not been agreed to by the competent authority, the virtual asset trading platform business may not provide trading platform services involving those virtual assets.

Image source: Made by Crypto City. Virtual Asset Services Act draft quick guide key points: Management compliance framework for virtual asset service providers

Key point 3: Regulations on issuing stablecoins in Taiwan

If a business wants to issue stablecoins within Taiwan, it should obtain permission from the competent authority, and the competent authority will consult with the Central Bank. The Executive Yuan’s version adds very strict red lines for stablecoins:

- Ban on paying interest and earnings: Stablecoin issuers may not pay interest or earnings in any form, and must issue and redeem at par value; the U.S.’s current stablecoin regulation “The Jane Act” also includes this provision.

- Reserves requirements and Central Bank penalties: Issuers must maintain sufficient reserve assets and keep them independently deposited. If reserves are insufficient, the Central Bank will impose a penalty by charging “interest at 5% per year on the insufficient portion” based on the minimum lending rate.

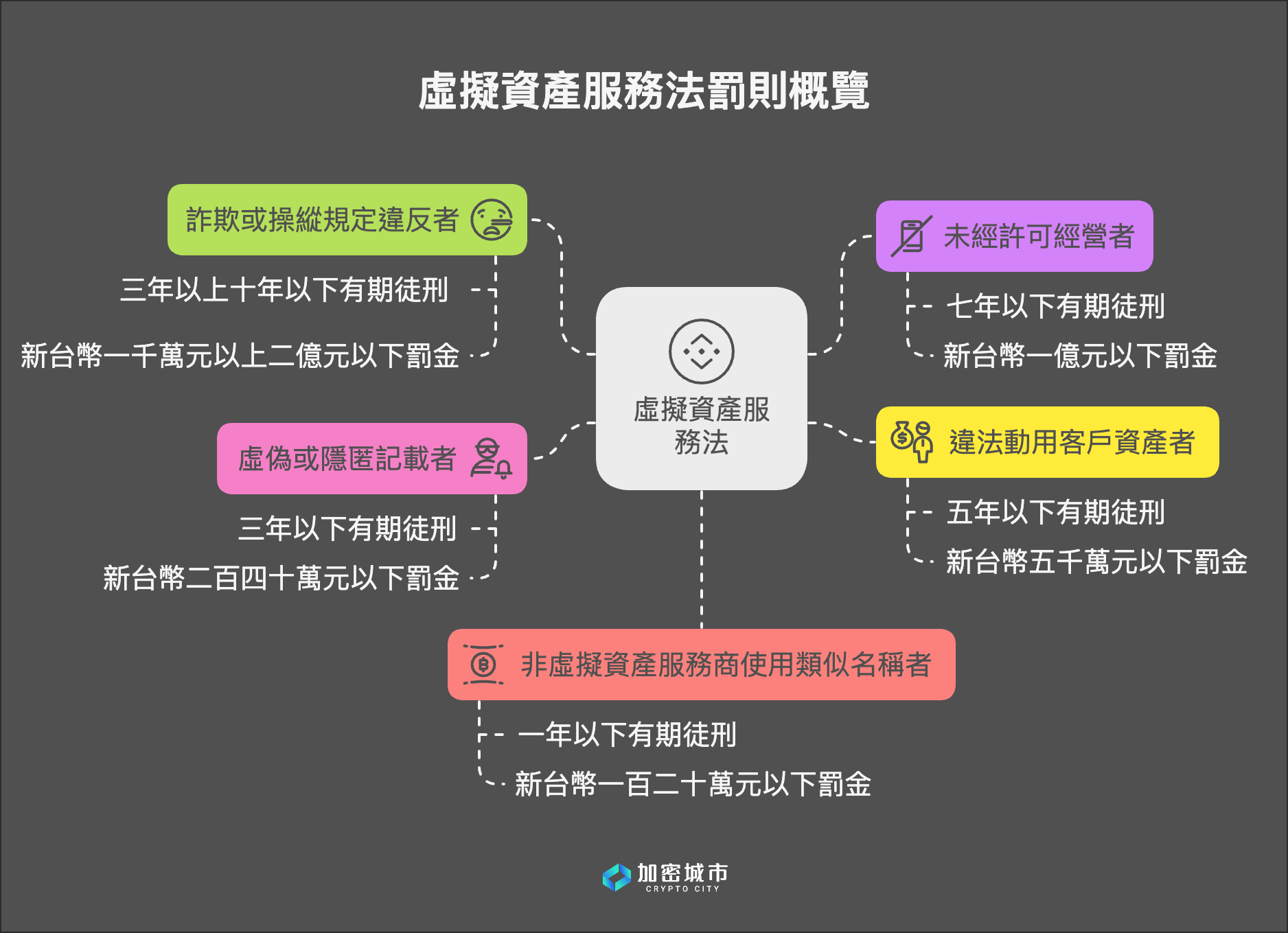

Key point 4: 8 major penalty provisions, with heavy penalties for fraud and market manipulation

The draft “Virtual Asset Services Act” imposes extremely severe penalties for acts such as fraud and market manipulation. The Executive Yuan’s version also significantly increases practical prosecution and follow-up mechanisms:

- Fraud or manipulation provisions: Imprisonment for not less than three years and not more than ten years, and may also impose a fine of not less than NT$10,000,000 and not more than NT$200,000,000.

- Plea of self-incrimination and admission leading to reduced punishment: For fraud or manipulation, if the offender pleads for mitigation (self-surrender) or admits guilt during investigation, and compensates the victims for the full amount within 6 months, the sentence may be reduced or exempted—to help investigators trace upstream sources.

- Operating without permission or issuing stablecoins: Imprisonment for not more than seven years, and may also impose a fine of not more than NT$100,000,000.

- Illegal use of customer assets: The responsible person will be punished with imprisonment for not more than five years, and may also impose a fine of not more than NT$50,000,000.

- Corporate dual-penalty mechanism: If an employee commits crimes such as operating without permission or unlawfully using assets, in addition to punishing the individual, the company (legal entity) will also be fined an equivalent high amount, such as up to NT$100,000,000 or NT$50,000,000.

- Hard labor conversion—harsher penalties: If the fine is more than NT$50,000,000, the term for conversion to hard labor is increased to no more than 2 years; if it is at least NT$100,000,000, it is increased to no more than 3 years.

- Confiscation of criminal proceeds: It is expressly stated that if the criminal proceeds are obtained by the offender or a third party, they should be confiscated except for returning them to victims.

- False concealment and misuse of names: Submitting an untruthful application, failing to provide reports, etc., is punishable by imprisonment for not more than three years or a fine of not more than NT$2.4 million; using a similar name by someone who is not a service provider is punishable by imprisonment for not more than one year or a fine of not more than NT$1.2 million.

Image source: Made by Crypto City. Virtual Asset Services Act draft quick guide key points: Supervision and penalties for virtual asset service providers

Controversy over the Virtual Asset Services Act: Can it balance protection + innovation?

The Financial Supervisory Commission said that, given that the U.S., the EU, Japan, South Korea, Hong Kong, and other places have gradually issued regulations related to virtual assets, international views on virtual asset oversight have increasingly converged. Therefore, based on ensuring Taiwan’s virtual asset business development, protecting investors, and also accommodating financial technology innovation, having a special law is necessary.

After undergoing revisions, this draft “Virtual Asset Services Act” has finally been formally approved by the Executive Yuan. The industry is also actively discussing it. Some positive views believe the regulations will help the industry become healthier, while opposing views argue that the provisions are extremely strict and may stifle startups.

However, it is worth noting that in this round, the Executive Yuan version also specifically added special clauses for “innovation experiments” and “international cooperation.” It stipulates that businesses may apply for innovation experiments (regulatory sandbox) and authorizes the competent authority to conduct cross-border information exchanges.

Overall, the coming into being of the “Virtual Asset Services Act” represents that Taiwan’s crypto-currency industry is officially moving from the era of frontier expansion to a more complete compliance and regulatory era—and businesses will inevitably face a period of pain that they have no choice but to endure.

News related to Taiwan’s virtual asset industry

- Planning for a New Taiwan dollar stablecoin? Capital Layer cooperates with Dunyang Technology; blockchain settlement will be introduced to banks

- Legislators raise the Bitcoin and stablecoin reserve strategy again! Yang Chin-long: stance remains unchanged for now, but time and space will change

- Can Taiwan’s stablecoins earn interest? The Legislative Yuan submits a legal-structure report on interest-earning stablecoins; the Financial Supervisory Commission has provided a preliminary response

- Binance wants to set up in Taiwan! Businesses worry about impacts on local crypto platforms; will a China-funded background affect national security?