👉#FDICReleasesStablecoinGuidanceDraft

The Stablecoin Guidance Draft, published by the Federal Deposit Insurance Corporation (FDIC), a key institution in the United States' financial regulatory architecture, represents a critical turning point for the global digital asset ecosystem. This draft guidance is considered one of the first comprehensive regulatory frameworks outlining how the relationship between the banking system and blockchain-based digital assets will be shaped.

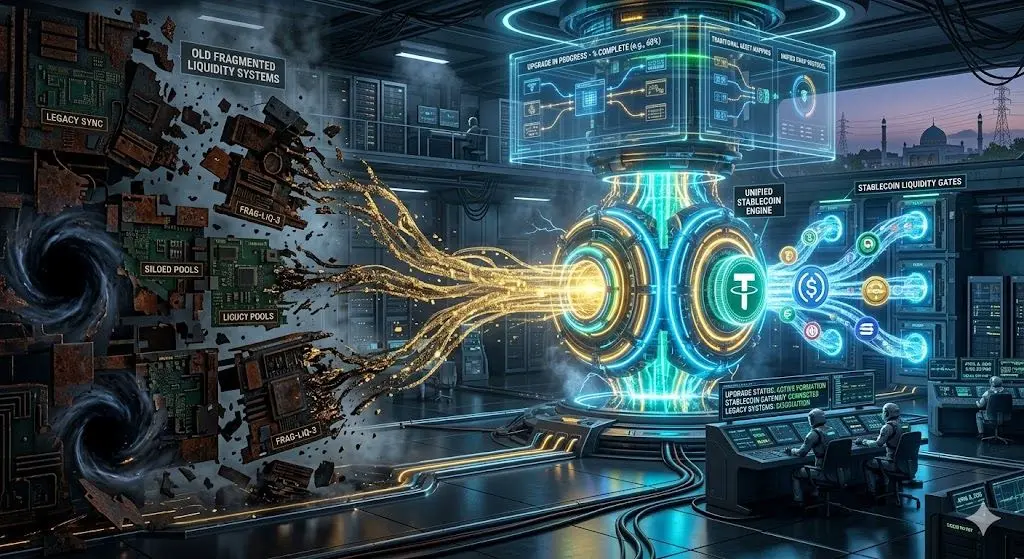

The stablecoin concept refers to digital assets whose value is typically pegged to fiat currencies. Assets such as USDC and Tether are widely used in global payment systems and decentralized finance applications. The draft guidance prepared by the FDIC aims to clarify the role of such assets within the banking system.

The primary objective of the draft document is to identify the risks that banks may face when issuing, holding, or offering services related to stablecoins, and to establish oversight mechanisms for these risks. In this context, liquidity risk, operational risk, cybersecurity risk, and consumer protection requirements are highlighted. Transparency of stablecoin reserves and the one-to-one correspondence principle are central to the regulatory approach.

The FDIC guidance also initiates an important discussion from a deposit insurance perspective. While deposits in the traditional banking system are insured up to a certain limit... Whether stablecoin assets will be included in this scope is not yet clear. The draft text adopts a cautious approach on this matter and emphasizes the obligation to provide clear information to prevent consumer deception.

The financial fluctuations experienced in recent years, and especially the collapse of algorithmic stablecoin projects, have been influential in the emergence of this development. As seen in the TerraUSD example, systems lacking sufficient reserves and oversight mechanisms can create serious systemic risks. Therefore, the draft guidance prepared by the FDIC is a reference not only for the US but also for global financial stability.

In terms of timing, this draft is not yet a final regulation and is open to public feedback. In this process, financial institutions, technology companies, and academic circles will contribute to shaping the final regulation by providing their views. In the medium term, it is expected that the guidance will be updated and transformed into binding regulations. In the long term, full integration of stablecoins with the traditional financial system may be possible.

From an economic perspective, such regulatory steps can play a confidence-building role in the markets. 😊 The increasing interest of institutional investors in digital assets is directly related to regulatory clarity. However, overly strict regulations can slow down innovation and lead to ventures facing different judgments. This could also lead to a shift in their regions.

Technologically and strategically, this guidance could directly affect the speed at which banks adopt blockchain technology. For traditional financial institutions, stablecoins offer significant opportunities in terms of cross-border payments, liquidity management, and digital asset custody services. Therefore, the FDIC approach is based not only on limiting risks but also on encouraging controlled innovation.

In conclusion, the Stablecoin Guidance Draft published by the FDIC stands out as one of the fundamental regulatory steps shaping the future of digital finance. 🌍 This draft heralds an era in which the boundaries between the banking system and crypto assets are being redefined. The final form of the regulation will be one of the critical factors determining the speed and direction of the digital transformation of the global financial architecture.

The Stablecoin Guidance Draft, published by the Federal Deposit Insurance Corporation (FDIC), a key institution in the United States' financial regulatory architecture, represents a critical turning point for the global digital asset ecosystem. This draft guidance is considered one of the first comprehensive regulatory frameworks outlining how the relationship between the banking system and blockchain-based digital assets will be shaped.

The stablecoin concept refers to digital assets whose value is typically pegged to fiat currencies. Assets such as USDC and Tether are widely used in global payment systems and decentralized finance applications. The draft guidance prepared by the FDIC aims to clarify the role of such assets within the banking system.

The primary objective of the draft document is to identify the risks that banks may face when issuing, holding, or offering services related to stablecoins, and to establish oversight mechanisms for these risks. In this context, liquidity risk, operational risk, cybersecurity risk, and consumer protection requirements are highlighted. Transparency of stablecoin reserves and the one-to-one correspondence principle are central to the regulatory approach.

The FDIC guidance also initiates an important discussion from a deposit insurance perspective. While deposits in the traditional banking system are insured up to a certain limit... Whether stablecoin assets will be included in this scope is not yet clear. The draft text adopts a cautious approach on this matter and emphasizes the obligation to provide clear information to prevent consumer deception.

The financial fluctuations experienced in recent years, and especially the collapse of algorithmic stablecoin projects, have been influential in the emergence of this development. As seen in the TerraUSD example, systems lacking sufficient reserves and oversight mechanisms can create serious systemic risks. Therefore, the draft guidance prepared by the FDIC is a reference not only for the US but also for global financial stability.

In terms of timing, this draft is not yet a final regulation and is open to public feedback. In this process, financial institutions, technology companies, and academic circles will contribute to shaping the final regulation by providing their views. In the medium term, it is expected that the guidance will be updated and transformed into binding regulations. In the long term, full integration of stablecoins with the traditional financial system may be possible.

From an economic perspective, such regulatory steps can play a confidence-building role in the markets. 😊 The increasing interest of institutional investors in digital assets is directly related to regulatory clarity. However, overly strict regulations can slow down innovation and lead to ventures facing different judgments. This could also lead to a shift in their regions.

Technologically and strategically, this guidance could directly affect the speed at which banks adopt blockchain technology. For traditional financial institutions, stablecoins offer significant opportunities in terms of cross-border payments, liquidity management, and digital asset custody services. Therefore, the FDIC approach is based not only on limiting risks but also on encouraging controlled innovation.

In conclusion, the Stablecoin Guidance Draft published by the FDIC stands out as one of the fundamental regulatory steps shaping the future of digital finance. 🌍 This draft heralds an era in which the boundaries between the banking system and crypto assets are being redefined. The final form of the regulation will be one of the critical factors determining the speed and direction of the digital transformation of the global financial architecture.