Author: RWA Industry Research Institute

Larry Fink, the CEO of BlackRock, officially acknowledged in his 2025 annual letter to shareholders that Bitcoin could challenge the dollar’s status as the global reserve currency. He warned that uncontrolled U.S. deficits could pave the way for Bitcoin to become the global reserve currency.

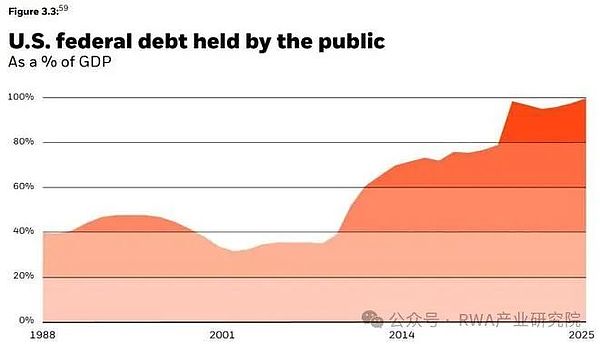

This letter clearly states that if the U.S. government cannot control its debt and deficit, Bitcoin is both a disruptive innovation and a geopolitical risk. The letter states: “If the U.S. cannot control its debt and if the deficit continues to expand, the U.S. could potentially hand over this status to digital assets like Bitcoin.”

( Source: BlackRock )

This statement marks the acknowledgment by the head of a $10 trillion asset management giant that digital assets can replace the dollar in the global market.

Fink mentioned Bitcoin 7 times and the US dollar 8 times in his letter. The importance of such a similar frequency in Fink’s annual letter cannot be overstated.

On January 11, 2024, the U.S. Securities and Exchange Commission approved BlackRock’s Bitcoin Spot ETF ( IBIT ), opening the door for traditional Wall Street investors to enter the digital asset space. Furthermore, U.S. President Trump has shifted to support Bitcoin, and the support for cryptocurrencies among domestic giants in the U.S. is gradually growing.

BlackRock’s letter outlines a divergent view, stating that although decentralized finance ( DeFi ) is praised as “an extraordinary innovation,” the company warns that its growth could undermine the dominance of the U.S. financial system.

The report emphasizes that risks could arise if investors begin to view Bitcoin as a more stable long-term store of value than the US dollar, especially in the context of ongoing US federal deficits and sovereign debt levels.

This framework positions Bitcoin not just as a speculative asset or a store of value, but as a macro hedge tool against the instability of U.S. sovereignty. Its implications are similar to arguments made by institutional investors in recent years, who view digital assets as insurance against currency devaluation or geopolitical turmoil.

As Finck emphasized, “two things can happen at the same time,” referring to the coexistence of innovation and risk in the development of digital assets.

BlackRock’s internal positioning on Bitcoin is not purely theoretical. The letter reveals that its Bitcoin spot ETF launched in the United States has become the largest product in the history of the ETF industry, managing assets over $50 billion in its first year. Among all ETF categories, it also ranks third in net asset inflows, only behind the S&P 500 index fund.

Retail adoption is the main driving factor, with over 50% of the demand for the company’s Bitcoin ETP coming from individual investors.

It is worth noting that 3/4 of the participants had never owned BlackRock iShares products before, indicating that Bitcoin is becoming an onboarding mechanism to attract a new group of investors.

The company has also expanded its ETP products to Canada and Europe, marking the cross-border growth of institutional-grade Bitcoin investment tools.

In addition to Bitcoin, Fink’s letter also presents a broader argument that tokenization can transform capital markets in a way comparable to the shift from postal services to email. Fink compares the tokenized asset infrastructure to the SWIFT network, arguing that the tokenized asset infrastructure can enable instant peer-to-peer asset flows, thereby bypassing traditional financial intermediaries.

BlackRock believes that tokenization represents a fundamental shift in asset ownership, primarily achieved through decentralization, improved voting systems, and increased opportunities for high-yield investment tools.

The letter states that these developments can reduce the operational and legal barriers that historically limited retail investors’ participation in certain asset classes, thereby democratizing capital markets.

The company also emphasized the necessity of updating the digital identity system, using the Indian model as a benchmark. According to the letter, over 90% of Indians can securely verify smartphone transactions, making the country a leader in the digital infrastructure necessary for a tokenized economy.

The inclusion of Bitcoin as a potential alternative to the US dollar reflects a significant shift in institutional thinking. While mainstream recognition of Bitcoin as “digital gold” has increased in recent years, BlackRock’s wording points to a deeper economic argument—failures in macroeconomic policy may accelerate the shift toward a decentralized monetary system.

By referencing tokenization and Bitcoin within the same strategic context, this letter presents a framework in which digital assets are potential systemic alternatives to fiat currency.

For policymakers, this information is subtle yet very clear: the United States must modernize its financial system and manage its debt trajectory to maintain its monetary leadership.

Disclaimer: The information on this page may come from third parties and does not represent the views or opinions of Gate. The content displayed on this page is for reference only and does not constitute any financial, investment, or legal advice. Gate does not guarantee the accuracy or completeness of the information and shall not be liable for any losses arising from the use of this information. Virtual asset investments carry high risks and are subject to significant price volatility. You may lose all of your invested principal. Please fully understand the relevant risks and make prudent decisions based on your own financial situation and risk tolerance. For details, please refer to

Disclaimer.